In the past, I have employed the “anti-bubble” framework developed by Nick Sleep and Qais Zakaria in the Nomad Letters as a basis for seeking out value. Last year, when energy was subdued while tech stocks skyrocketed, I redirected my attention to technology. Now that conditions have reversed and energy seems to be at a peak based on fundamentals, I am looking again to tech with renewed interest. There is a sell-off occurring in my preferred tech stocks due to a decrease in digital advertising and e-commerce revenues.

The quartet of Alphabet Inc. (NASDAQ:GOOG, NASDAQ:GOOGL) (“Google”), Amazon (AMZN), Meta Platforms (META), and Microsoft Corporation (MSFT) stands out as the cream of the crop in terms of capital allocation by management. This is evidenced by their impressive ROIC and high-profit margins; when a section of the market is affected, these are the best companies to look for at a fair discount to their historical values. Although Apple Inc. (AAPL) could be included too, its chart remains defying gravity.

Alphabet Inc., like Meta, derives most of its revenue from digital ad sales. As long as some amazing venture capitalist comes up with an acceptable way to implant a chip in our heads and beam ads directly to us, I think digital advertising will continue to grow. The economy will slow, but when it snaps back, look out. Google and Meta are going to go on a hiring spree again once that fulcrum hits.

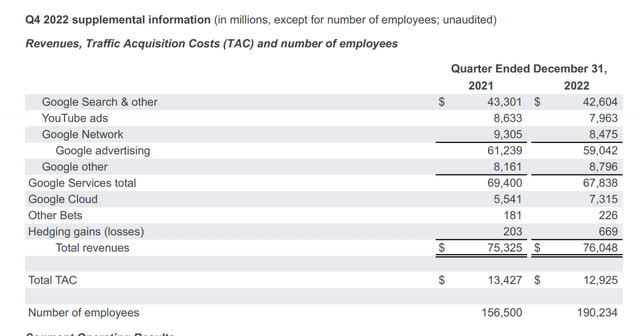

The Alphabet top line numbers for Q4 2022 are also available here. With ad revenue down a couple of billion dollars and cloud services up a couple of billion dollars to offset that decline, total revenues came in slightly ahead of 2021. Google’s revenue is flat, with the most positive item being the 32% increase in cloud services revenue. Alphabet still had 33,734 more employees at the end of 2022, even after layoffs.

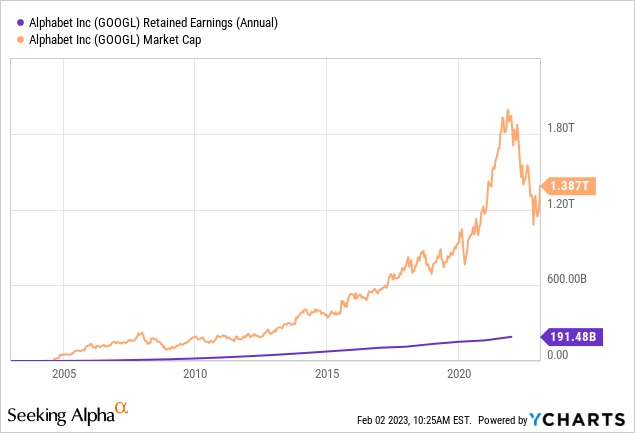

The return to the investor from Alphabet Inc. is primarily through retained earnings and the growth of its holdings and businesses, in the same way that Berkshire Hathaway (BRK.B, BRK.A) does. This, like Berkshire, is one of the few stocks that do not pay dividends, so we have to trust them with their capital allocation decisions.

Google/Alphabet’s TTM EBITDA is currently at $93.733 Billion and with 13.242 Billion shares outstanding, the company has an EBITDA of $7.078 per share. Applying an 17.8x multiple to this yields a price target of $120.89 - pushing it close to the upper-end but still within value parameters. As many companies have lots of R&D and tax benefits, non-GAAP under-the-hood methods are my favoured method of calculation when examining growth figures; although there has been a slight slowdown from the previous assessment.